ACT tax reform program on track

The ACT Government is committed to raising revenue in a way that is fair, efficient and sustainable, delivering the resources we need to fund great public services for Canberrans.

Our 20-year tax reform program is now approaching the half-way point, delivering real benefits for Canberrans and a more stable revenue base to fund essential services for our community in the years to come.

Through tax reform we have already:

- Abolished insurance duty – saving a household with $3,000 worth of insurance $300 a year

- Raised the ACT’s payroll tax threshold to $2 million – meaning 90 per cent of ACT small and medium businesses now pay no payroll tax

- Cut stamp duty to zero for commercial property transactions worth $1.5 million or less – meaning around 70 per cent of commercial property transactions now involve no stamp duty.

From 1 July this year we will fully abolish stamp duty for eligible first home buyers, no matter whether they are purchasing a newly-built home or an existing one in an established suburb.

Around 2,000 Canberra first home buyers a year will benefit from more choice and lower upfront costs when buying their own home.

And we will continue to cut stamp duty rates for all home buyers – just as we’ve done in every Budget since 2012-13.

- The buyer of a $500,000 residential property will now pay $9,100 less in stamp duty than when tax reform commenced.

- The stamp duty charge for a $500,000 property in the ACT in 2019-20 is $11,400 compared with $17,990 in NSW and $21,970 in Victoria.

How does it work?

We are shifting the ACT’s tax mix away from narrowly-based transaction taxes towards a broad land tax base through general rates.

Tax reform commenced in 2012-13, and is being delivered in several five-year stages. We will reach the halfway mark of this reform program during the current Budget forward estimates period.

Before the start of each stage, we announce the cuts to stamp duty rates for the coming five year period, and also set the target average annual general rates increase for residential and commercial properties.

The reform program is broadly revenue neutral over time, with the reductions in revenue from phasing out stamp duty being replaced through gradual increases in general rates.

Data from the Australian Bureau of Statistics shows that since tax reform commenced, the ACT’s overall growth in revenue from general rates, conveyance duty and insurance tax combined has been both below the Australian average and significantly lower than New South Wales or Victoria.

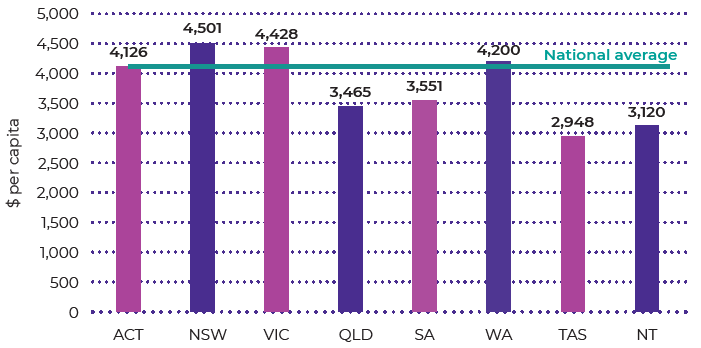

The ACT’s tax per capita rate remains comparable to the Australian average and is also lower than across the border in New South Wales. Through tax reform we are changing the ACT’s tax mix – not increasing the overall tax take.

Total own-source tax revenue per capita (2017-18)

The ACT remains an attractive place to live and do business while we implement tax reform. This is demonstrated by the fact that our population is growing by over 8,000 people a year and 3,246 net new businesses have started up in Canberra in the past four years.

What’s new?

The Government plans to release the settings for the next five-year phase of tax reform as part of the 2020-21 Budget.

To assist with this, we have commissioned a detailed analysis of the impacts of tax reform so far on Canberra’s economy, our revenue base and Canberrans across the income distribution.

The analysis will be conducted over the coming year with assistance from a Tax Reform Advisory Group made up of independent experts and ACT Treasury. This detailed work will help inform the settings for the next five-year phase of tax reform commencing in 2022-23.

Introducing separate rating factors for houses and unit titled homes

From 2019-20 we will introduce different rating factors for standalone houses and unit titled residential properties.

This responds to community feedback on changes that were made to the method for calculating unit rates as part of implementing the current stage of tax reform.

- Having two sets of rating factors ensures unit owners can be charged according to a progressive scale for rates, while maintaining an equitable approach to calculating rates for all residential properties.

- Residential general rates for houses will increase by an average of 7 per cent in 2019 20. For unit titled properties, rates will increase by an average of 11 per cent as we continue the transition to the calculation methodology which commenced in 2017-18. This transition will be smoothed by a further year to support the implementation of separate unit rating factors.

Smoothing commercial rates changes

General rates are levied based on the Average Unimproved Value of a block of land. At the moment, this is calculated as a three-year rolling average of the unimproved land value.

Because of the way Canberra is changing and the growing number of urban renewal sites across the city, some commercial properties have seen big year-to-year changes in their underlying land value. This can flow through to unexpectedly large changes in annual commercial rates.

To help smooth out the impact of changes in land value on commercial rates, from 2020-21 we will lengthen the time period used for calculating Average Unimproved Values for commercial properties. These changes will be implemented in consultation with industry over the coming year, to deliver more predictable rates bills for commercial property owners.

For more information on the ACT Government’s tax reform agenda see Chapter 6 of the 2019-20 ACT Budget Outlook.